Today, I’d be surprised to hear anyone advise founders to “grow at all costs.”

But we’ve been through cycles where that was 100% the case. I’ve lived the experience a few times.

In 2021, I was involved with several startups that were given clear instructions (by others) to, “Spend! Spend! Spend!” By early 2022 the message had flipped completely, “Cut! Cut! Cut!” For inexperienced founders this is particularly difficult to navigate—you trust your investors & board, want to react accordingly and demonstrate you’re listening. You go overboard on the burn, only to find support has fallen out from under you, and you have to overcorrect.

These stories are common. And they happen every boom-bust cycle.

The latest “trend” is founders claiming they can get to profitability after one round of financing. I have no doubt this is possible in some cases, but it begs the question, “Are you building a venture-profile business?”

VCs don’t want to hear you’ll take their money, scrimp and save, and grind to profitability, because that sounds like it’s going to take a long time and not generate big, juicy returns. The irony of raising capital is that it generally only leads to one place: raising more capital. What VCs really want to hear is that you’ll raise now and in the near future you’ll raise more at a higher valuation (making them look like geniuses, and giving them good “paper returns”).

Once you get on the hamster wheel of venture capital it is very difficult to jump off.

The pressure to grow and spend and raise (at higher valuations!) is significant.

So should you bootstrap instead?

Not necessarily, although you certainly can.

Bootstrapping is a completely viable way to build certain types of businesses. If you’re operating a business that doesn’t require a lot of initial capital (or you’re comfortable self-funding with your own money) and can generate revenue (+ profit!) quickly, bootstrapping makes sense. Side hustles often fit into this category, but a bootstrapped business does not have to be small.

Mailchimp was bootstrapped. They hit $600M ARR in 2018 and in 2021 were acquired by Intuit for ~$12B in stock & cash.

Here’s an awesome interview with Ben Chestnut, CEO/Founder at Mailchimp, about his journey.

Zoho is another incredible example.

They do over $1B in ARR

They reach 100M users

They’ve raised $0.

In 2010, Sridhar Vembu, CEO/Founder at Zoho wrote a blog post about why they’ve never taken venture capital.

“First, let me state that I don't have any fundamental religious issues with venture capital. I know many VCs personally well, and I respect what they do. I have just come to believe that VCs necessarily have different priorities and different motivations than people who create and operate businesses.

What is the primary difference? Ultimately it comes down to the question of "exit". As a founder, I have no interest in exit or liquidity. I am in business to run a business, not to run away from it. Or as Warren Buffet puts it: Our favorite holding period is forever.”

Bootstrapping a business doesn’t mean it costs nothing to start or run. You’ll have to be able to self-fund it. And it’ll likely take longer to scale because you won’t have any additional capital to fuel growth; you’ll eat what you kill and recycle every possible dollar back into the business. Bootstrapping is not for the faint of heart.

You can bootstrap and then raise venture capital

Some very successful startups bootstrapped initially and then raised venture capital.

Shopify started in 2006, but didn’t raise capital for 4 years. The company raised a small angel round at the beginning of 2010 and then $7M Series A near the end of that year.

Github started in 2008, but didn’t raise capital until 2012 when they received $100M from Andreesen Horowitz and SV Angel. 😝

Wayfair started in 2002, but didn’t raise capital until 2011, securing $165M from Battery Ventures and Great Hill Partners

These are incredible stories. Huge wins. And ultimately they were all venture-profile businesses that raised hundreds of millions of dollars once they had proven traction and business models.

If you can bootstrap to a certain level of traction / success / validation before raising, it makes sense. You don’t get on the VC hamster wheel too quickly and don’t spend too aggressively to grow in the early days.

In 2018 Eric Paley wrote a great article in TechCrunch: When venture capital becomes vanity capital. He compares companies that bootstrapped (or raised less / later) versus those that got hooked on the VC money drug. He makes a good argument for being cautious about raising too much capital (especially too quickly).

More capital does not always equal better returns (although some times more capital is a key to winning)

You can’t fundraise your way to victory alone

But if others outspend you smartly, they can beat you

This is why there’s no perfect answer to, “How much capital should I raise and when should I raise it?”

When I worked at VarageSale, we raised ~$30M from top-tier investors (Sequoia and Lightspeed). It was an incredible feeling. But the pressure to grow at all costs was massive and we couldn’t crack it, despite having a version of product-market fit that was compelling.

Product-Market Fit: What does this actually mean?

A lot of founders declare product-market fit much too early. At VarageSale we never specifically said, “We have PMF!” but it sure felt like we did. The product was incredibly sticky, with 40% DAU/MAU (which means 40% of our monthly active users used VarageSale daily). That’s what led us to raise ~$30M. We were growing at a decent clip, but because of the nature of the business (small, closed communities to buy & sell) we didn’t have hyper-growth. We’d acquire buy & sell communities one at a time and get them onto the VarageSale platform. Each one would grow independently, but because they were closed and often geographically constrained, individual communities never became massive.

I do think we had product-market fit — but that wasn’t enough for us to win, which was a painful lesson, and one I see a lot of founders go through, especially when they falsely declare PMF early and assume everything is going to go smoothly in terms of fast growth going forward.

VarageSale’s competitors ended up raising way more than us (OfferUp had raised ~$215M & LetGo had raised ~$375M by the time VarageSale exited in 2017) which put even more pressure on us to spend / burn and try to grow. LetGo was acquired/merged with OfferUp, which is still in existence—I have no clue if they’ll actually win and generate a return, but they definitely beat out smaller players (like VarageSale).

Raising too early may lead to a bridge round (or two)

A lot of founders want to raise capital right out of the gate. Maybe it’s a necessity because you don’t have the funds to bootstrap (which I completely understand). The risk of raising very early is that you don’t get far enough to justify the next round at a higher valuation. When that happens you find yourself having to take bridge rounds at flat or lower valuations. Or you try to bootstrap your way through to a better growth trajectory (so you can raise more funding later).

Raising early puts you onto a specific trajectory: raising more. The likelihood of raising once (especially very early) and never raising again is small. You’ll want to spend to grow, and your investors will almost certainly pressure you to do so.

If you’re going to take money early, make sure it’s from people you genuinely trust or people who are incredibly passive (or both). You do not want helicopter investors, or investors that turn on you when things go sideways (btw, they always go sideways).

Inception Investing is Hot

Despite my warnings above, I’m a believer in what is now being called “Inception Investing.” It’s what we do at Highline Beta as a venture studio. We call it “Formation Capital.”

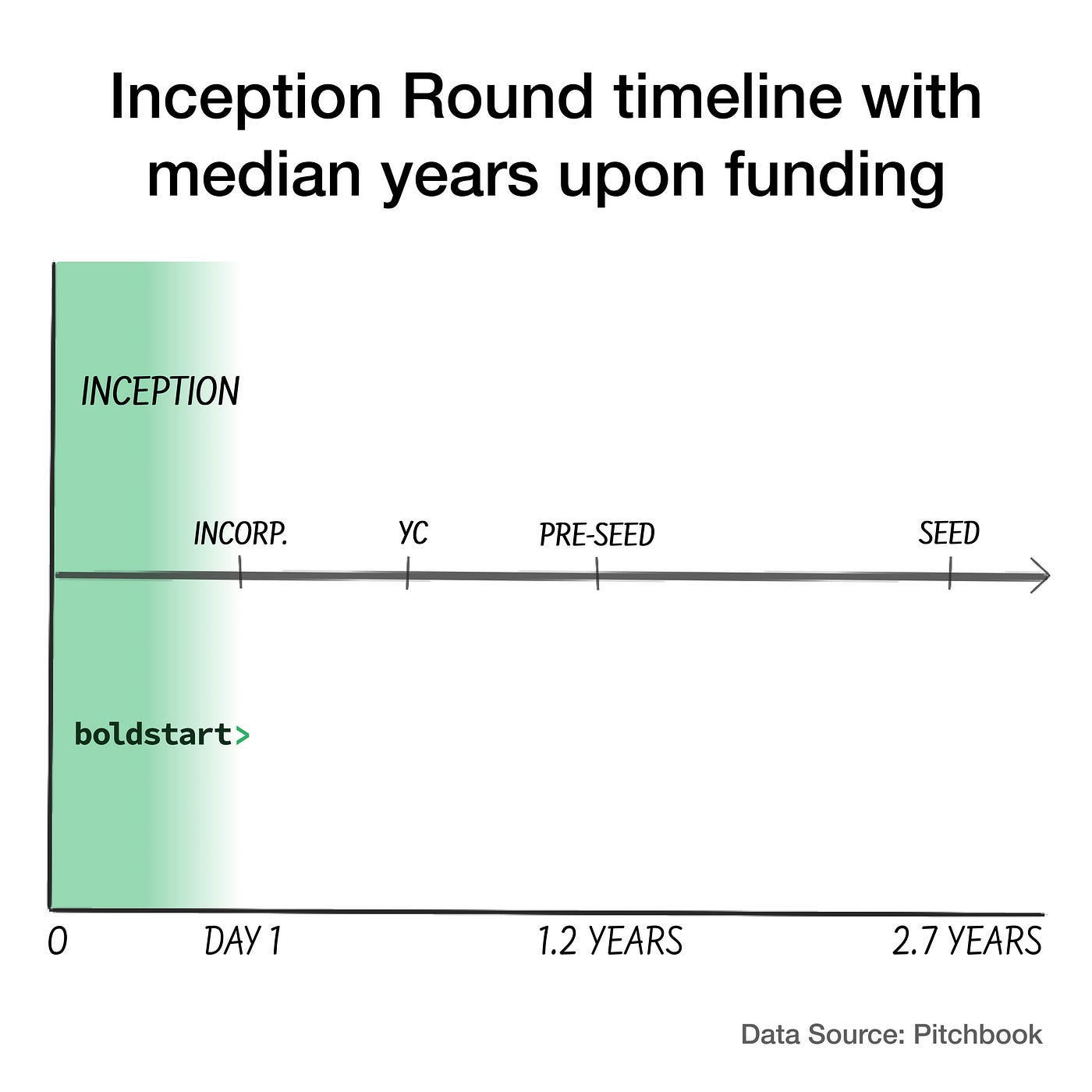

Ed Sim, Founder and Managing Partner at boldstart ventures (B2B enterprise investor) is extremely bullish on super early investing, at incorporation, before a pre-seed round comes together.

He recently wrote an awesome article about inception investing and its growing popularity. Some highlights:

“Inception investing is the most competitive area of VC at the moment which means in order to win one must compete with angels, pre-seed firms, seed funds, and multi-stage firms in the 3 types of rounds.”

“‘Inception Investing’ means engaging with founders well before they incorporate, helping them battle test and iterate those ideas, helping them pre-sell some of the initial hires, and leading those rounds upon company formation so founders can run fast out of gates and not spend months trying to raise capital. It’s been happening for quite some time and is not constrained by any dollar amount.”

Ed includes a great visual on when inception investing takes place versus other rounds:

I’m a big believer in Inception Investing and supporting founders with hands-on support. That’s the definition of a venture studio. But it’s also the riskiest time to invest and it can put founders on a “raise more money forever” path.

Where does that leave a founder trying to figure all of this out?

It’s easy to run around in circles trying to decide on the best strategy. Here’s a thought exercise that may help:

1. What does winning look like for you?

When you start a company there are only a few positive outcomes (excluding failure and a fire sale):

Win really, really big ($500M+ exit to IPO)

Win small (but still generate a return)

Build a “lifestyle business”

You may not know which one you want as an outcome, but if you do, ask yourself, “Why?” A lot of people automatically gravitate towards “win really big!” but when pressed aren’t willing to admit why they chose that answer.

Most founders will say “I wanna win big” almost by default. Any other answer is often looked down upon. Does that make sense? Of course not.

But it’s easy to get caught in the hype and believe that swinging for a home run is the only way to build a startup. It might be the only way to convince investors, but it’s clear VC capital isn’t the only path to success.

Some founders aim big but end up with a smaller, meaningful exit. I’ve seen this numerous times and it can be absolutely life changing for the founders & early employees. Plenty of founders make more money on an early exit than a later one, because they own more of the company. Investors don’t love it because they’re not getting a “fund returner.” Angels may be super happy with it. Venture studios also benefit from smaller exits because of the higher percentage equity they take early on—suddenly the base hits and doubles make a big difference and you need less home runs to generate real returns.

But it’s tough to raise capital pitching a “small win.” It’s not something VCs want to hear. Others (angels, studios, etc.) may be open to starting a business with a smaller exit in mind, but there has to be a strong strategic component to the investment that increases the odds of an early exit (a slow, small exit is bad!)

Exits are never guaranteed, so shooting low seems strange, and you can see why it doesn’t work for VCs. But that may not be the case in the context of a vertical venture studio, where you can increase the odds of identifying real, painful problems, securing customers and getting to market faster.

Vertical venture studios should be able to more successfully and repeatably manufacture early, positive exits.

2. Can you self-fund the first 1-3 years to launch a product and get initial traction?

Most people aren’t in a position to do this, unless it’s a side hustle. That’s unfortunate because it sets them on a specific path of seeking external capital, almost above anything else (such as validating the problem, building the right solution, targeting the right customer, proving value, etc.)

Fundraising becomes the business.

It’s partially why funding rounds are celebrated so voraciously, because we know how hard it is to raise capital and it feels like a big milestone. It is, but raising capital gives founders a false sense of security and victory (neither of which are true when you raise money).

If you can self-fund for awhile and get a product launched with traction, you may find fundraising easier because you’ve further de-risked the business. It also shows investors your level of commitment.

Venture studios are emerging to bridge the gap between founders self-funding + grinding independently and “later stage” venture capital. Money alone isn’t always enough to accelerate the creation and early progress of a startup (i.e. Inception Investing without any real support). Venture studios are meant to roll-up their sleeves and help build startups, de-risking further and providing a powerful launchpad.

3. Are you OK ceding (some) control and operating more professionally in exchange for capital?

You may want / need capital, but aren’t prepared for the repercussions or expectations that come with fundraising.

Selling a piece of your company means you’re giving up some degree of control. Each time you raise money, you give up a bit more control. Some founders manage to maintain majority control for a very long time, but it’s not common. Understanding the terms by which you accept money is critical to understanding what you’re exchanging for that money.

Once you raise from investors (which may include angel investors / angel groups, not just VCs) there are certain expectations for how you’ll run the business and how you’ll report on progress. You’ll have a Board of Directors (that doesn’t just include the founder(s), where you’ll have to do things “by the book”. Your performance will be reviewed and discussed. You are now responsible for more people than yourself, and your investors will expect you to operate the business professionally.

Selling a portion of your startup and operate it professionally aren’t bad things, but you need to go into them eyes open. If you can’t stomach the idea of either, raising capital isn’t a good idea.

4. Do you genuinely understand the path you’re going on once you’ve raised money (from different sources)?

I’m a big believer in optionality. Linear paths rarely work. You want to maintain as many options as possible for winning, without under-committing to the path that you believe has the best chance.

Fundraising decisions have a big impact on increasing or reducing optionality.

Raising from VCs (especially early on) sets you on an expected path of hyper-growth and ever-increasing valuations. (btw, neither of these things are inherently bad, they’re just forcing functions on the type of startup you build and how you make decisions). Ed Sim pointed out the trend of later-stage VCs getting into much earlier stage investing (including at inception), which sounds great, unless those VCs aren’t prepared for the risk and nebulous nature of starting companies. Most startups grow slowly in the first few years, bumbling around trying to figure things out, and they need capital partners that truly understand that.

Bootstrapping sets you on a slower path, because you have fewer resources. It comes with a lot more independence, but may also be much riskier for founders (since they’re taking on all the financial burden). If you can get a product to market with early traction, you can shift from bootstrapping to raising venture capital (it’s much more difficult to go the other way, although not impossible).

Working with a venture studio may be the “best of both worlds” although it comes with its own challenges. A venture studio should provide capital + support at inception, which de-risks things for you as the founder. Studios should speed up the first few messy years (validating a problem, building a solution, getting traction), and make it an easier journey, which arguably should lead to better quality startups emerging. But, depending on the cap table (some studios take 40-50%+ upfront), you may find raising future capital (especially if you decide you want/need venture capital for hyper-growth) much more difficult. Venture studios may be viable “off-ramps” to early exits / smaller wins, because the incentives are more aligned (through the cap table) than if you raise from VCs alone, but again, if you own too little of the startup, an early exit may not be a meaningful financial windfall.

No matter which path(s) you choose, pick your partners wisely. Breaking up with investors is basically impossible. Make sure you understand the pros and cons of the financing decisions you’re making, so you can do what you believe is in the best interests of your startup (and hopefully you as well). 🙏

Thanks for reading! I need your help. I’ve started receiving great questions from readers, which end up becoming the inspiration for my newsletter.

If you have any questions, please let me know! I’ll respond (as quickly and effectively as I can) and never publish anything in the newsletter without your permission.

Thanks for reading Focused Chaos! Subscribe for free to receive new posts and support my work.

When I'm searching for inspiration all I have to do is come to Focused Chaos and read. Thank you again Ben. Glad to add Inception Investing into the vocab

When I'm searching for inspiration all I have to do is come to Focused Chaos and read. Thank you again Ben. Glad to add Inception Investing into the vocab